What to Do Before You Cancel

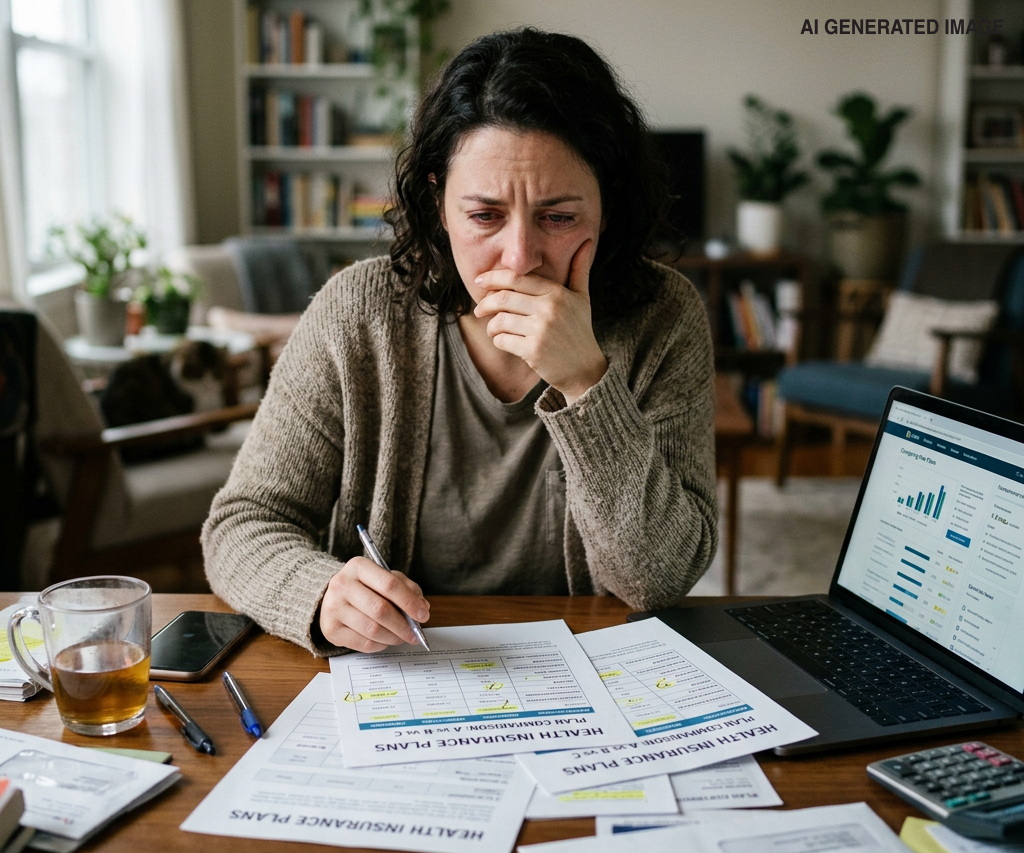

Health insurance costs can feel overwhelming, especially when premiums, deductibles, or everyday expenses start to stretch your budget. If you’re enrolled in an ACA (Affordable Care Act) Marketplace plan and thinking about canceling it because it feels unaffordable, you’re not alone.

But before you make that decision, it’s important to pause. Canceling your plan without exploring your options can leave you exposed to high medical costs and limit your ability to re-enroll later. In many cases, there are better solutions available, and a licensed insurance agent can help you find them.

Here’s what to do if your ACA plan no longer feels affordable.

1. Don’t Cancel Your Plan Right Away

It might seem like canceling your coverage is the quickest way to save money, but it can create bigger problems down the road.

If you cancel:

- You may

lose access to financial assistance (subsidies)

- You could be

uninsured for months until the next Open Enrollment Period

- A medical emergency could result in

significant out-of-pocket costs

Instead of canceling immediately, take time to explore your options.

2. Review Your Current Subsidy (You May Qualify for More Help)

Many people don’t realize that ACA subsidies (premium tax credits) are based on your

current income, and if your income has changed since your enrollment, your savings might not be accurate anymore.

You may qualify for:

- Lower monthly premiums

- Reduced deductibles and copays (if eligible for cost-sharing reductions)

- Expanded subsidies under recent federal updates

A small change in income, like reduced work hours or job changes, can increase your financial assistance. It is important to update your ACA application and see if increased financial assistance is available.

3. Talk to a Licensed Agent or Broker

This is one of the most important steps.

A licensed insurance agent can:

- Review your

current plan and costs

- Check if you qualify for

additional savings

- Help you compare

more affordable plan options

- Guide you through

plan changes or Special Enrollment Periods

Best of all, working with an agent typically

costs you nothing. Their services are compensated by insurance carriers, not you.

Many people find that simply speaking with an agent uncovers options they didn’t know existed.

4. See If You Qualify for a Special Enrollment Period

Outside of Open Enrollment, you can only change plans if you qualify for a

Special Enrollment Period (SEP).

Common qualifying events include:

- Loss of income

- Change in household size (marriage, divorce, birth)

- Moving to a new coverage area

- Loss of other health coverage

If your household or financial situation has changed, you may be eligible to

update your application and switch to a more affordable plan.

5. Consider Adjusting Your Plan (Instead of Dropping Coverage)

If your current plan is too expensive, you may be able to:

- Switch to a

lower-premium plan

- Choose a plan with a

higher deductible but lower monthly cost

- Reevaluate your coverage level (Bronze, Silver, Gold)

Even a modest adjustment can make your plan more manageable while still protecting you from major medical expenses.

6. Explore Medicaid Eligibility

If your income has dropped significantly, you may qualify for

Medicaid, which offers low-cost or no-cost coverage.

Eligibility varies by state, but many people are surprised to find they qualify after a change in income.

An agent can help you:

- Determine eligibility

- Assist with the application process

- Transition coverage smoothly if needed

7. Understand the Risks of Going Without Coverage

It’s tempting to go without insurance to save money, but the risks are real.

Without coverage:

- A single hospital visit can cost

thousands of dollars

- Preventive care and prescriptions become more expensive

- You may delay needed health care, leading to

worse health outcomes

Health insurance is designed to protect both your

health and your finances.

You Have Options

If your ACA plan feels unaffordable, you’re not stuck, and you’re not alone. There are often solutions available that can lower your costs without sacrificing coverage.

The key takeaway is simple:

Don’t cancel your plan without speaking to a licensed agent first.

A quick conversation could help you:

- Save money

- Improve your coverage

- Avoid gaps in insurance

When it comes to your health and financial security, it’s worth exploring every option before making a decision.